Products Search Address:111 Middle Yangzi Road, Yangzhong, Jiangsu, China Tel:86-511-88320021 Fax:86-511-88328972 E-mail:sixiaofeng@hotmail.com |

HOME >> NEWS >> The development status of domestic and foreign pet industry

一、The development of foreign pet industry

In developed countries, the pet industry has experienced more than 100 years of development, forming an industry system composed of pet supplies, pet food, pet breeding, pet medical treatment, pet training, pet insurance and other products and services, and has formed a relatively mature market.

The pet market in developed countries has become an important part of their national economy. According to Euromonitor statistics, the global pet market in 2017 was nearly 120 billion U.S. dollars, and it is growing at a rate of about 3.5% per year. North America is the largest consumer of the global pet market.

1 American market

The pet industry has a history of more than 100 years in the United States, but it only entered the industrial development track around the 1980s. According to the changes in the characteristics of the pet industry, it is divided into three periods: the 1980s to the early 21st century is the incubation period of the industry; the early 21st century to the first ten years of the 21st century is the rapid development period; the beginning of 2010 is the period of industrial integration.

The United States is the world's largest pet raising and consumption country. Pet keeping has become an important part of Americans' lives. According to data from the American Pet Products Association ("APPA"):

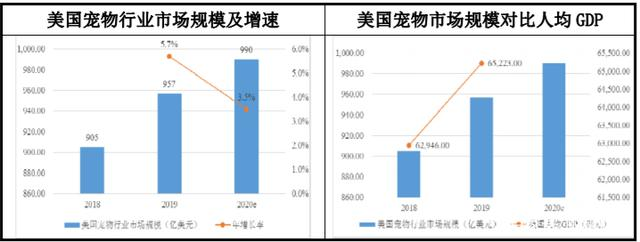

The market size of the US pet industry in 2019 is approximately US$95.7 billion, an increase of approximately 5.7% compared to US$90.5 billion in 2018. It is expected that the market size of the pet industry in 2020 will reach US$99 billion. From a data point of view, the size of the US pet market has grown with the growth of American per capita GDP. This is because rapid economic development will, on the one hand, increase the average consumption of pets; on the other hand, it will also increase the number of people who are able to keep pets. In 2019, the proportion of households with pets in the United States reached 67%. Among them, pet dogs are the most popular pet breed, with a household ownership rate of 50%; followed by pet cats, which account for 34% of households; and the ownership rate of other pets is below 10%.

2 European market

Europe is another major pet consumer market in the world. Similar to the US market environment, the European pet industry is relatively mature after years of development. Statistics from the European Pet Food Industry Federation (FEDIAF) show that the pet industry still contributes a lot to the overall economy. The annual output value of the pet economy has increased from 36.5 billion euros in 2017 to 39.5 billion euros in 2018, an increase of 82%.

In 2018, the total number of pet cats and dogs in European countries was 189 million, of which the number of cats was about 103.83 million and the number of dogs was about 85.18 million. In Europe, Russia is the largest pet consumer country, and the number of pet cats and dogs is much higher than that of Germany, France, Britain and other countries. Number of cats and dogs in major European countries in 2018 (ten thousand)

3 Japanese market

The pet industry started early in Japan. With the increase in the number of breeders, the richness of pet-related products and services has greatly increased. The development of the Japanese pet industry can be roughly divided into three periods: the beginning period before the 1970s and 1980s; the growth period from the 1970s and 1980s to the 21st century; and the mature period from the 21st century to the present.

According to data released by Yano Economic Research Institute, the Japanese pet industry market size was 1,449.8 billion yen in 2014. Since then, the market size has increased steadily year by year, reaching 1,544.2 billion yen in 2018. It is expected that the pet industry will maintain a steady growth trend in the future. The market size is expected to reach 1,625.7 billion yen in 2021, with an average compound growth rate of approximately 165% during 2014-2021.

Japan's pet industry market size

Due to the high population density in Japan, apartments are the most common residence. Therefore, animals that are small in size and suitable for indoor breeding account for a relatively high proportion. Pets are increasingly playing the role of children and partners in the lives of breeders to meet their emotional needs, and breeders' willingness to consume has also increased. Although Japan's per capita GDP has declined after 2012, it has not affected Japanese pet owners' consumption demand for pets.

二、The development of China's pet industry

China's pet industry has developed relatively late. Since the 1990s, China's pet industry has entered a period of accelerated development. With the development of China's population structure and economy, China's population aging has intensified, and the only child area has gradually become the main consumer. The gradual increase in the number of elderly people in our country and the new generation of young people are more advocating the free life of living alone, and the need for companionship of pets has increased, and the role of pets has gradually changed from "care home care" to "emotional companionship".

1 The domestic pet industry market develops rapidly

The development of China's pet market has benefited from the growth of per capita GDP, the development of the central and western regions, and the expansion of groups living alone. It is currently in a period of rapid development.

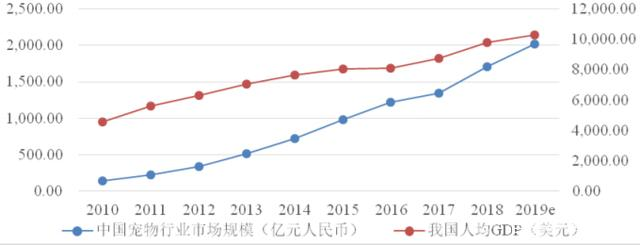

According to the data of the White Paper on China's Pet Industry in 2019, the size of China's pet market in 2019 is about 202.4 billion yuan, an increase of 18.5% year-on-year, and the average compound growth rate from 2010 to 2019 is about 34.55%. China's pet industry is in a period of rapid development, and the brand awareness of breeders is gradually increasing. The "blowout era" of the pet industry has arrived.

The market size of China's pet industry

2 Cats and dogs are still the main pets, but the types of pets are diversified

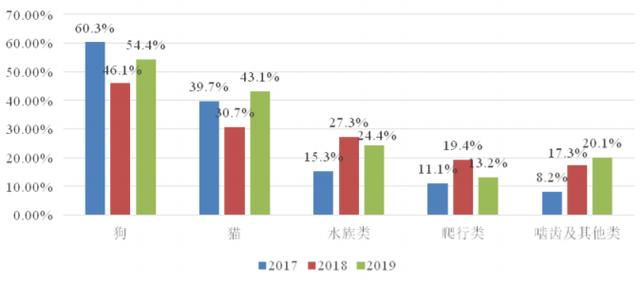

Currently, cats and dogs still dominate the pet category. According to the data of the White Paper on China's Pet Industry in 2019, 43.1% and 54.4% of breeders regard cats and dogs as pets respectively, and the proportion of pet owners of aquariums, reptiles, rodents and other categories has reached 24.4%, respectively. 13.2% and 20.1%. It can be seen that the pet selection and preference of breeders are more diverse.

Proportion of various types of pets in China's pet industry

3 The consumption amount of a single pet is growing rapidly

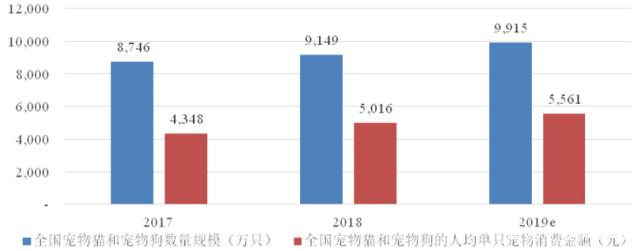

According to the data released by the White Paper on China's Pet Industry in 2019, the number of pet dogs in cities and towns across the country reached approximately 55.03 million in 2019, an increase of approximately 8.2% compared to 50.85 million in 2018; the number of pet cats reached approximately 44.12 million , Compared with 40.64 million in 2018, an increase of approximately 8.6%;

In terms of pet consumption level, the annual consumption of a single pet dog per capita in China in 2019 is about 6,082 yuan, which is an increase of about 9.0% compared to 5,580 yuan in 2018; the annual consumption of a single pet cat per capita is about 4,755 Yuan, compared with 4,311 Yuan in 2018, an increase of approximately 10.3%. As shown below:

The scale of the number of pet cats and pet dogs in China and the amount of consumption per pet per capita

4 The population of first-tier and second-tier cities is the main force for pets

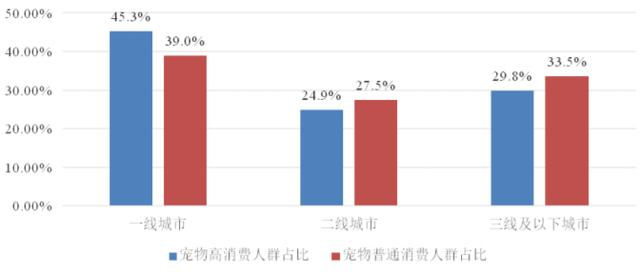

First-tier and second-tier cities are still the main battlefields for pet consumption, but the potential for pet consumption in third-tier and lower cities is huge. According to the survey statistics of the "White Paper on China's Pet Industry in 2019", among the high pet consumers (based on a monthly consumption of more than 500 yuan as a staple pet food), the first-tier cities accounted for 45.3%, the second-tier cities accounted for 24.9%, and the third-tier cities accounted for 45.3%. Cities and below accounted for 29.8%; for general pet consumers, first-tier cities accounted for 39.0%, second-tier cities accounted for 27.5%, and third-tier cities accounted for 33.5%. In the future, China's third-tier and lower cities are expected to become an important driving force for the continued increase in the market size of the pet industry.

The proportion of high pet consumption and general consumption groups in various tier cities in China

|